from diffrax import (diffeqsolve, ControlTerm, Euler, MultiTerm,

ODETerm, SaveAt, VirtualBrownianTree)

t0, t1 = 0., 1.

def drift(t, y, args):

S, V = y

r, V0, k, theta, sigma, rho = args

d_y = jnp.array([r * S, k * (theta - V)])

return d_y

def diffusion(t, y, args):

S, V = y

V = jnp.maximum(V, 0.001)

r, V0, k, theta, sigma, rho = args

mixing = jnp.array([[1., 0.],

[rho, jnp.sqrt(1-rho**2)]])

scale = jnp.diag(jnp.array([jnp.sqrt(V)*S,

jnp.sqrt(V)*sigma]))

return scale @ mixing

brownian_motion = VirtualBrownianTree(t0, t1, tol=1e-3,

shape=(2,), key=jr.PRNGKey(0))

terms = MultiTerm(ODETerm(drift),

ControlTerm(diffusion, brownian_motion))

solver = Euler()

saveat = SaveAt(dense=True, ts=jnp.linspace(0., 1., 2000))

args = (0.05, 0.04, 5., 0.16, 0.9, 0.1)

sol = diffeqsolve(terms, solver, t0, t1,

dt0=0.001, y0=jnp.array([1.0, 0.04]),

args=args, saveat=saveat, max_steps=20000)Stochastic differential equations and numerical methods

In my previous post, I discussed stochastic differential equations (SDE) and presented a method to estimate the time-dependent probability density function \(p_t(x)\) of their solution \(X_t\). It relied on masked autoregressive neural networks trained on samples of \(X_t\) generated by a numerical integrator. I briefly mentioned that in a lot of applications, these samples can be used directly to compute Monte Carlo estimates of quantities of interest. For instance, the risk-adjusted net present value of a clinical development program was calculated with this method in the post on risk management and investment decisions, where I argued that implementing it in a differentiable programming library such as JAX facilitates the computation of sensitivities.

This approach is also used in the finance industry to compute the value of derivative instruments, when the time-evolution of the underlying asset price is modelled with a stochastic differential equation. This SDE can be calibrated by matching statistics of historical data (for instance the mean and variance of log-returns in the case of a geometric Brownian motion), through direct statistical inference with a discretized model (see the post on Gaussian random walks), or by reproducing the market prices of liquid derivatives, typically vanilla options.

As a side note, mathematical finance considers two types of probability measures, namely real world measures for risk management, and risk-neutral measures for arbitrage-free asset pricing. Calibrating an SDE to historical data produces a real world model that can be used to compute the risk exposure of an investment portfolio, with metrics such as the value at risk. Calibrating it to market prices of liquid derivatives on the other hand produces a risk-neutral model that can be used for the valuation of less liquid instruments such as exotic over-the-counter derivatives.

In practice, the model calibration to market prices is often implemented by converting the SDE into an equivalent partial differential equation formulation, and deriving from there an integral formula of the derivative prices. Its parameters are then varied to match the observed market prices. The SDE is finally used with these calibrated parameters to generate samples for Monte Carlo pricing methods.

The reason for using an integral formula for the parameter calibration rather than Monte Carlo estimates directly is that efficient calibration relies on gradient-based methods, and computing the gradients of Monte Carlo estimates with respect to the model parameters can be difficult. The pain point is the backpropagation of gradients through the numerical integration of the SDE. On the other hand, deriving an integral formula works only for special cases of SDE such as the Back-Scholes model or the Heston model, but is in general cases a very hard problem.

This is where recent numerical integration libraries such as torchsde or Diffrax come in handy as they implement backpropagation through integration with adjoint methods and make the calibration of arbitrary SDE models possible.

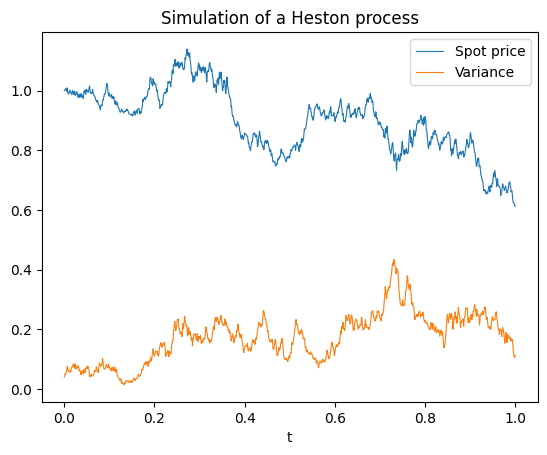

Heston model

As an example, we can consider the Heston model

\[ \begin{align*} dS_t &= r\, S_t \, dt + \sqrt{V_t} S_t \, dW_t^S, \\ dV_t &= k (\theta - V_t) \, dt + \sigma \sqrt{V_t} \, dW_t^V, \\ dW_t^S\, dW_t^V &= \rho \, dt. \end{align*} \]

Specifying its SDE only takes a few lines of code in Diffrax. Note how the correlation \(\rho\) is introduced as a mixing matrix of two independent Wiener processes.

The drift and diffusion functions take t and y as inputs, which are the time and two-dimensional state of the SDE, and args, which packs the parameters of the model. For calibration, the goal is to build a scalar loss function that depends on these parameters and minimize it through gradient descent.

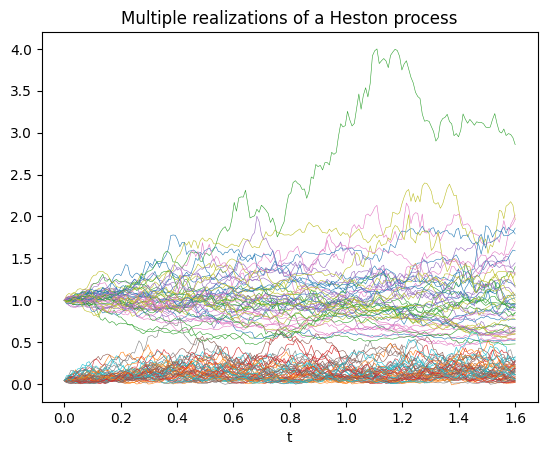

Functions that involve pseudo random number generation in JAX always require their own key, so to simulate several realizations of a stochastic process, it is best to build a function that depends on a key argument, and map it to as many keys as required with jax.vmap. Here it is wrapped in a simulate function to keep track of the dependence on the parameters in args and specify with a SaveAt object at which time points we want to record the stochastic process. To plot trajectories, we want it to be dense, but to price European options, we want to record only the states at the relevant maturities of the contracts.

t0, t1 = 0., 1.6

t_size = 200

ts = jnp.linspace(t0, t1, t_size)

saveat = SaveAt(ts=ts)

def simulate(args, saveat, dataset_size=100):

@jax.jit

@jax.vmap

def get_data(key):

bm_key, vol_key = jr.split(key, 2)

bm = VirtualBrownianTree(t0, t1, tol=1e-3, shape=(2,), key=bm_key)

drift_term = ODETerm(drift)

diffusion_term = ControlTerm(diffusion, bm)

terms = MultiTerm(drift_term, diffusion_term)

solver = Euler()

dt0 = 0.005

r, V0, k, theta, sigma, rho = args

y0 = jnp.array([1.0, V0])

sol = diffeqsolve(

terms, solver, t0, t1, dt0, y0, saveat=saveat, args=args

)

return sol.ts, sol.ys

seed = 123

key = jr.PRNGKey(seed)

data_key = jr.split(key, dataset_size)

ts, ys = get_data(data_key)

return ts, ys

Option pricing

As an illustration (inspired by the MATLAB documentation), we can calibrate this model to a European call option chain.

spot_price = 123.28

strikes = jnp.array([115., 120., 125., 130., 135., 140., 145])

maturity_dates = [datetime.strptime(s, '%Y;%m;%d') for s in

['2015;8;21', '2015;9;18', '2015;12;18',

'2016;4;15', '2016;6;17', '2017;1;20']]

settle_date =datetime.strptime('2015;7;10', '%Y;%m;%d')

maturities = jnp.array([(md.date() - settle_date.date()).days/365

for md in maturity_dates]) #time to maturity in years

market_calls = jnp.array([

[9.95, 10.63, 12.84, 15.1, 15.95, 20.0],

[6.3, 7.2, 9.9, 12.3, 13.57, 17.5],

[3.6, 4.55, 7.3, 9.7, 11.15, 15.2],

[1.82, 2.68, 5.3, 7.7, 9.0, 13.2],

[0.82, 1.45, 3.7, 5.85, 7.2, 11.27],

[0.36, 0.77, 2.5, 4.48, 5.76, 9.65],

[0.15, 0.38, 1.7, 3.44, 4.54, 8.1]])The first step is to compute the price of these options under the Heston model. So we simulate the value of the spot price at the different maturities, we compute the option payoff for every strike price, and we return the discounted Monte Carlo mean as the option prices. Here, instead of specifying the risk-free rate, we will compute its implied value. The initial value of the variance V0 is unknown, so we will also learn it from the option market prices. This is why these two parameters are included in the args parameters. On the other hand, the initial spot_price is an input, but we had \(S_0 = 1\), so we need to multiply the simulated \(S_t\) by spot_price to get the proper price evolution.

@jax.jit

def compute_call_price(spot_price, args, strikes,

maturities, sample_size=512):

ts, ys = simulate(args,

SaveAt(ts=maturities),

dataset_size=sample_size)

spot_price_at_maturity = spot_price*ys[...,0]

r, V0, k, theta, sigma, rho = args

discount = jnp.exp(-r*maturities)

simulated_payoffs = jnp.maximum(

spot_price_at_maturity[:,None] - strikes[...,None], 0)

simulated_calls = discount * jnp.mean(simulated_payoffs,

axis=0)

return simulated_callsCalibration

For calibration, we need to penalize discrepancies between the simulated option prices and their market values. Here we choose the (unweighted) mean squared relative error. Taking the relative rather than absolute error is motivated by the fact that these option prices cover three orders of magnitude, and we want to avoid too big an influence from the options that are deep in the money. In practice, we might also introduce weights that depend on the bid-ask spreads to reflect different uncertainties in market prices. The result is a loss function that depends as required only on the args parameters.

@jax.jit

def compute_loss(args):

simulated_calls = compute_call_price(spot_price,

args,

strikes,

maturities)

errors = simulated_calls - market_calls

msre = jnp.mean((errors/market_calls)**2)

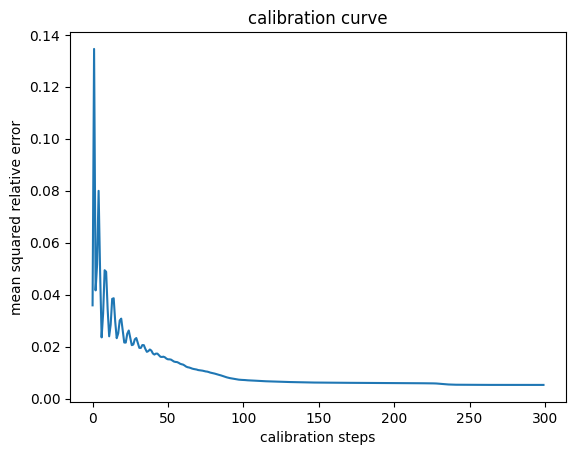

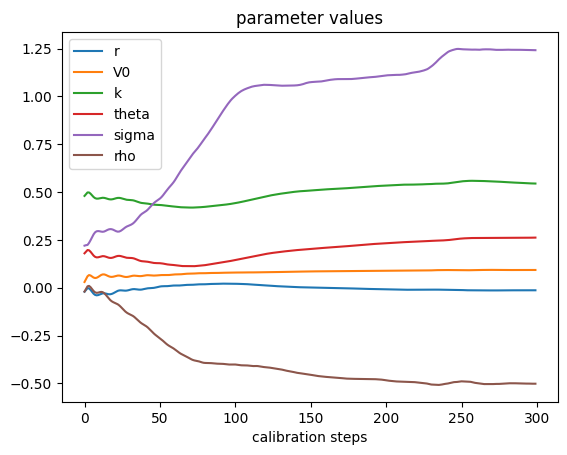

return msreTo find the parameters that minimize this mean squared relative error and provide the best fit to the market prices, we use the Optax library. This works because the gradients nicely backpropagate through the entire implementation of compute_loss, including the diffrax.diffeqsolve numerical integrator.

params = jnp.array([-0.001, 0.05, .5, 0.2, 0.2, 0.])

start_learning_rate = 0.02

optimizer = optax.adam(start_learning_rate)

# Initialize parameters of the model + optimizer.

opt_state = optimizer.init(params)

history = []

msres = []

for _ in range(300):

value, grads = jax.value_and_grad(compute_loss)(params)

updates, opt_state = optimizer.update(grads, opt_state)

params = optax.apply_updates(params, updates)

history.append(params)

msres.append(value)

The initial “half-piping” of the calibration curve could be avoided with a learning rate scheduler, and it could speed up convergence, but the key takeaway is that this method converges and produces a well-calibrated interpretable stochastic model.

As a final sanity check, one can compare the calibrated call prices with the market values.

Calibrated call prices:

[[ 9.99 11.4 13.5 14.9 16.23 19.97]

[ 6.5 7.91 10.3 11.89 13.34 17.28]

[ 3.68 4.9 7.62 9.32 10.79 14.9 ]

[ 1.77 2.78 5.5 7.22 8.63 12.84]

[ 0.76 1.57 3.9 5.5 6.87 11.05]

[ 0.3 0.85 2.73 4.27 5.53 9.5 ]

[ 0.12 0.45 1.95 3.32 4.51 8.22]]

Market call prices:

[[ 9.95 10.63 12.84 15.1 15.95 20. ]

[ 6.3 7.2 9.9 12.3 13.57 17.5 ]

[ 3.6 4.55 7.3 9.7 11.15 15.2 ]

[ 1.82 2.68 5.3 7.7 9. 13.2 ]

[ 0.82 1.45 3.7 5.85 7.2 11.27]

[ 0.36 0.77 2.5 4.48 5.76 9.65]

[ 0.15 0.38 1.7 3.44 4.54 8.1 ]]Conclusion

This example demonstrated how easy it is to automatically calibrate an SDE to expected values such as derivative prices in differentiable programming frameworks like JAX or PyTorch. Moreoever, these frameworks natively support hardware acceleration and parallelization, so these workflows can be scaled up with minimal effort. Practioners no longer need to stick to simple models like Black-Scholes, but can quickly experiment with more realistic models that better capture features of the processes they work with.